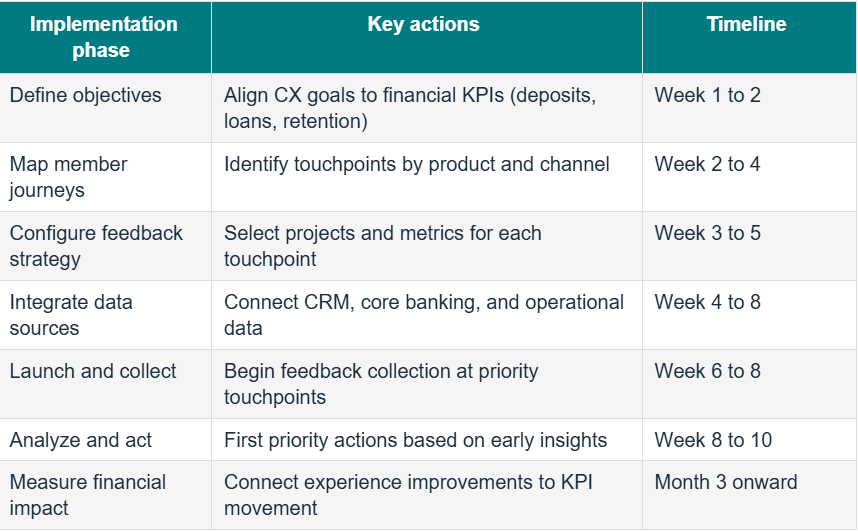

Strategy only delivers value when it is implemented. A well-designed experience management framework sitting on a slide deck is worth nothing. The question is how a credit union moves from recognizing the importance of connected experience intelligence to building the infrastructure that makes it real.

Implementation does not have to be a massive, multi-year transformation. The most effective approaches start with clear financial objectives, map the member journeys where those objectives live, and build a measurement system that connects feedback to outcomes. To create a detailed roadmap for credit unions to meet their business objectives, we used the Experience Navigator, a Sogolytics tool designed to make that progression structured and tractable.

Step 1: Start with the financial objective, not the metric

The most common mistake in experience management implementation is starting with a project and hoping useful insights emerge. A more effective approach starts with a financial objective and works backward to the experience touchpoints that influence it.

If the objective is a 10% increase in funded loan volume, the relevant touchpoints are the digital application form, the underwriting communication process, the loan officer consultation experience, and the disbursement workflow. These are the places to measure, and the feedback collected there should be designed to answer specific questions about where friction is costing loans.

If the objective is deposit growth among new members, the relevant touchpoints are the onboarding process, the digital banking enrollment experience, and the welcome communication quality. Different objectives, different touchpoints, and different feedback designs.

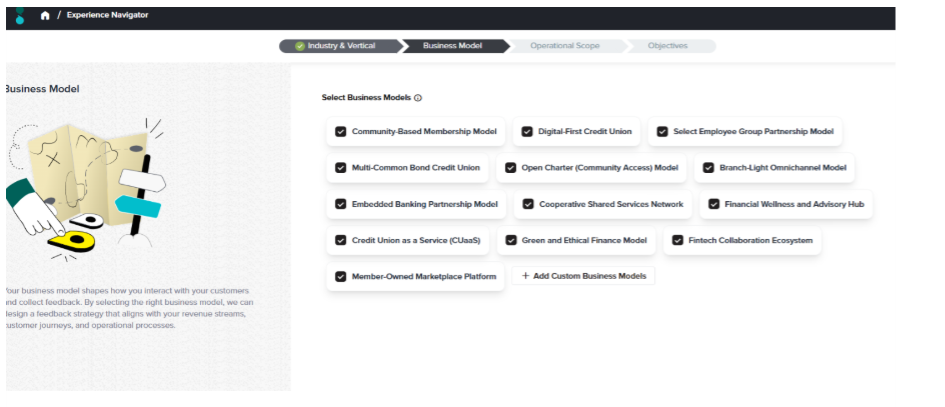

Experience Navigator guides credit unions through business model and operational scope selection to align feedback strategy with institutional priorities.

Step 2: Map the member journey with specificity

Generic member journey maps are of limited value. Account opening, loan application, service recovery, digital engagement: these high-level stages need to be broken into specific touchpoints before they can be measured and improved.

Account opening, for example, contains at least six distinct touchpoints: the online membership application portal, the welcome email communication, the in-branch account opening session, the identity verification and compliance process, the account activation workflow, and the member service representative interaction. Each one has its own potential friction points, and each one requires its own feedback approach.

Experience Navigator does this mapping work systematically, identifying digital, physical, process, and human touchpoints for each objective and recommending targeted projects for each.

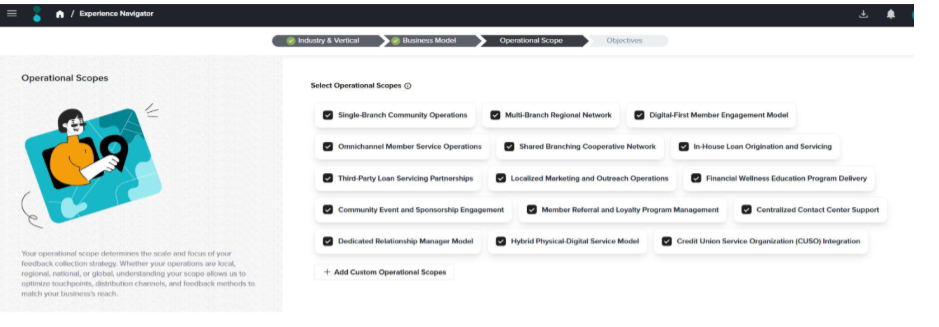

Operational scope selection in Experience Navigator ensures the feedback strategy matches the credit union’s actual service delivery model.

Step 3: Integrate data sources to create a connected view

Experience data in isolation has limited strategic value. The power comes from connecting it to what the institution already knows about members. CRM data that shows product relationships. Core banking data that shows balance trends and transaction frequency. Operational data that shows complaint volumes and resolution times.

When a member who scores low on digital banking satisfaction is also showing declining balance activity and has not logged into online banking in three weeks, that combination of signals is far more actionable than any individual data point. Building the integrations that allow this kind of connected analysis is a technical investment, but it is the infrastructure that transforms experience management from a reporting function to a strategic one.

Step 4: Build the governance model

Implementation without governance produces data that never gets acted on. Someone needs to own each experience metric, understand what drives it, and have the authority and accountability to change it. Without this, even excellent insights expire unused.

Effective governance does not require a large team. It requires clear ownership, a regular cadence of action-focused review, and a shared language between CX teams and the financial leaders they report to. Sogolytics’ dashboard and alerting infrastructure is designed to support this, making sure that the right people see the right signals at the right time to act before opportunities are lost.

Create a Member Experience Customized to Your Credit Union’s Unique Goals

Every credit union operates within a distinct set of member relationships, service commitments, and financial priorities. A community development credit union serving first-time borrowers faces different experience challenges than a digital-first institution competing for younger members on mobile. The framework above applies across both, but the specific touchpoints, objectives, and feedback design will look different for each.

Experience Navigator is built for exactly that variation. Rather than applying a generic project template and hoping the results are useful, it guides your team through a structured process that starts with your actual business model, maps the member journeys that matter most to your institution, and recommends a feedback strategy calibrated to your operational scope. The output is not a report to file away. It is a working system that connects what members are telling you about the financial outcomes your leadership is accountable for.

Ready to move from recognizing the importance of member experience to building the infrastructure that acts on it?