Most banks operate on the assumption that competitive rates and rewards programs are the primary levers for customer loyalty. The Sogolytics CX Rankings: U.S. Banking 2026 challenges that assumption with hard numbers.

Sogolytics surveyed 1,018 U.S. consumers about their everyday banking experiences across Bank of America, Citibank, JPMorgan Chase, Wells Fargo, and U.S. Bank. The study measured ease, speed, digital self-service, branch experience, trust, and overall satisfaction, then mapped those factors to loyalty and switching intent. The findings are a practical primer on where customer experience gaps are forming and what banks need to fix before those gaps cost them relationships.

Digital is the Default. Not a Feature.

Banks have long treated digital investment as a younger-customer play. Build a strong app, capture millennials and Gen Z, and let the rest of the customer base do what it has always done. The data from this study does not support that framing.

Across all five banks surveyed, 50% of customers say they primarily bank through digital channels. Another 35% describe themselves as hybrid users who combine digital tools with occasional branch visits. Only 15% bank mostly in person. More telling: even among respondents aged 65 and older, 46% report banking mostly digitally. The assumption that older customers are branch-dependent does not hold at the scale this study captures.

What this means in practice is that digital experience is no longer a feature a bank can optimize for one segment. It is the primary channel through which most customers, across generations, form their day-to-day impression of their institution. A slow app, a confusing website flow, or an ATM experience that takes more steps than it should; these are not edge-case friction points. They are the experience, for the majority of customers, most of the time.

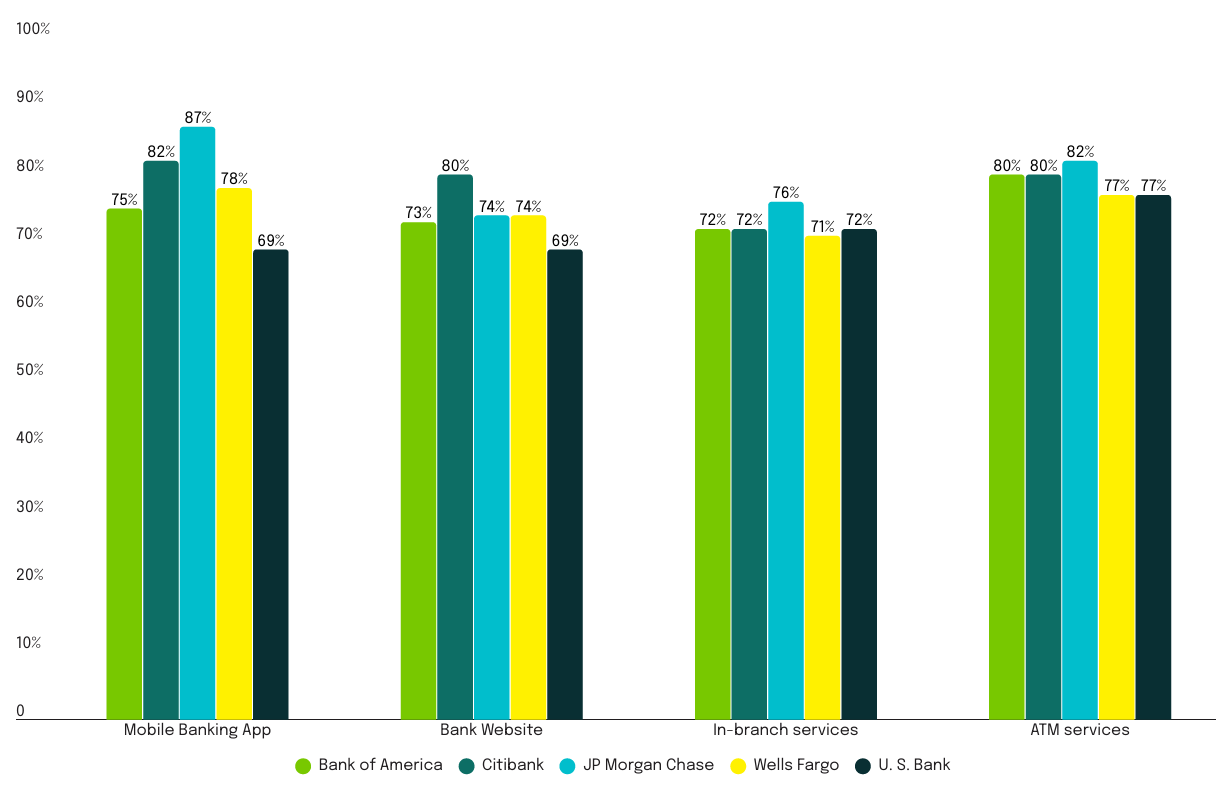

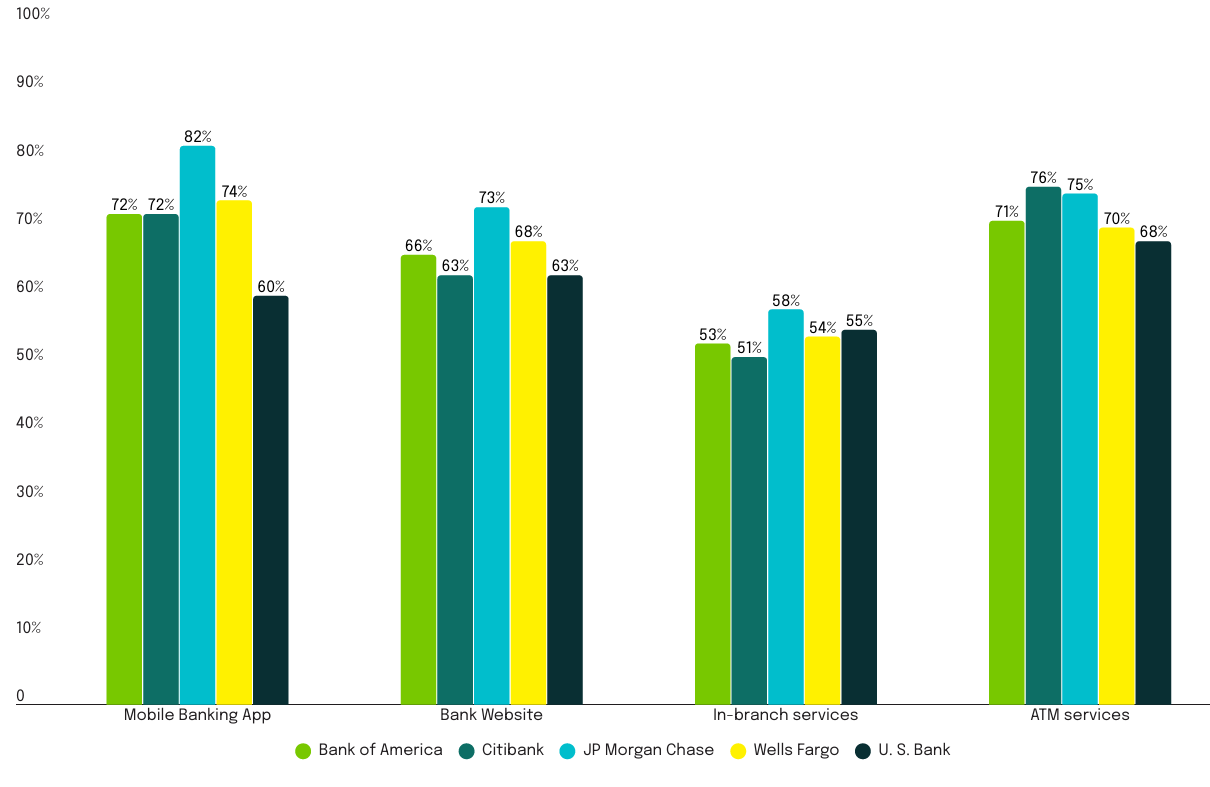

The data on ease and speed reinforce this point. JPMorgan Chase ranks first in mobile app ease, with 87% of its customers finding everyday tasks easy or very easy to complete in the app. It also leads on mobile app speed, with 82% rating app-based tasks as fast or very fast. These are not marginal advantages. For a customer trying to transfer funds on a Monday morning, a slow or confusing app is a friction point that compounds over time.

(Sogolytics CX Rankings: U.S. Banking 2026): Ease of completing everyday banking tasks across mobile app, website, in-branch, and ATM channels. JPMorgan Chase leads on mobile app ease at 87%.

(Sogolytics CX Rankings: U.S. Banking 2026): Speed of completing everyday banking tasks across all channels. JPMorgan Chase leads mobile app speed at 82%; in-branch speed scores are markedly lower across all institutions.

For banks and credit unions evaluating their digital experience, this is where measurement needs to start. Our guide to customer effort scoring walks through how financial institutions can begin quantifying the friction customers experience across channels.

The Loyalty Drivers Banks Keep Underestimating

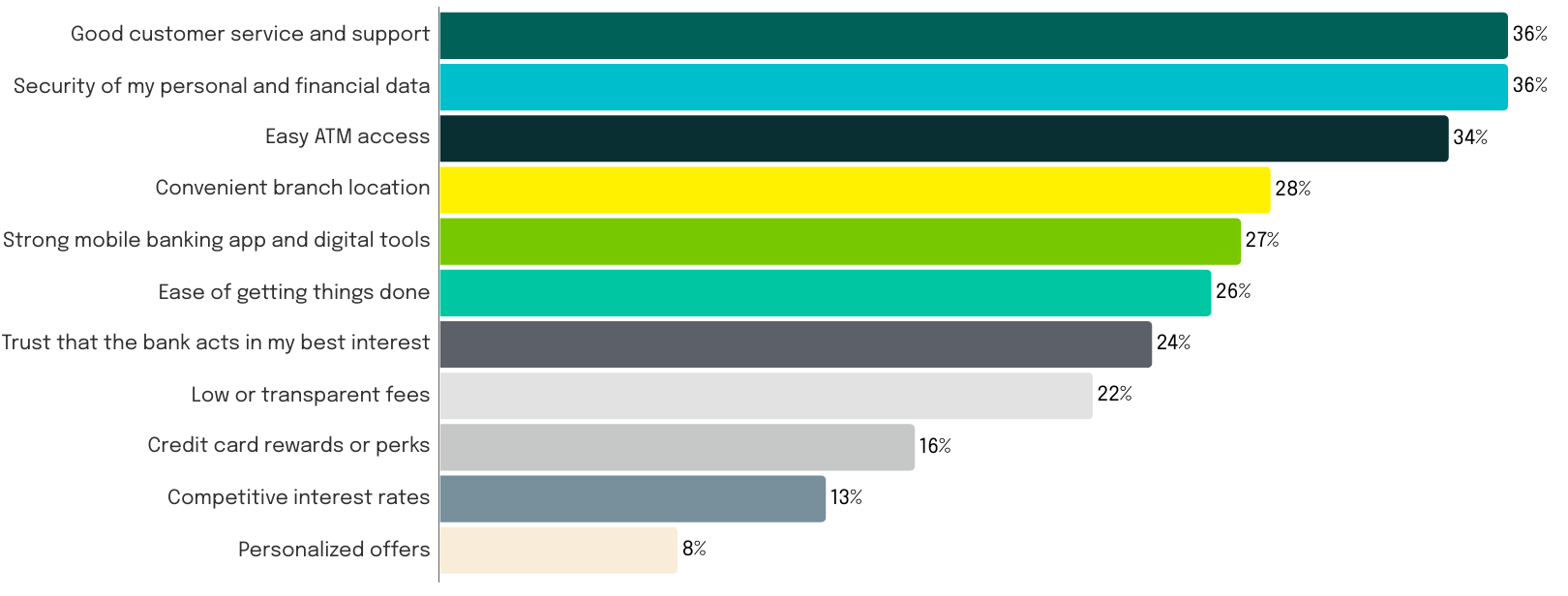

When the study asked consumers what they value most when choosing a bank, the top two answers were good customer service and support (36%) and security of personal and financial data (36%). Easy ATM access came third at 34%.

Strong mobile banking app and digital tools ranked fifth, at 27%. Competitive interest rates landed near the bottom at 13%. Personalized offers came last, at 8%.

(Sogolytics CX Rankings: U.S. Banking 2026): Factors customers value most when choosing a bank. Customer service and data security tie at 36%, well ahead of interest rates (13%) and personalized offers (8%).

This ranking matters, because it directly contradicts where many banks invest their CX budgets. Rewards programs, cashback offers, and rate promotions are visible and measurable in the short term. But when customers are choosing whether to stay or leave, the experience of getting things done, feeling served quickly, and trusting that their data is protected carries significantly more weight.

This is consistent with what we see in broader consumer experience data. The Sogolytics Experience Index: Customer Edition 2026 shows that effort and reliability are among the strongest predictors of loyalty intent across industries.

Effort is the Hidden Friction Cost

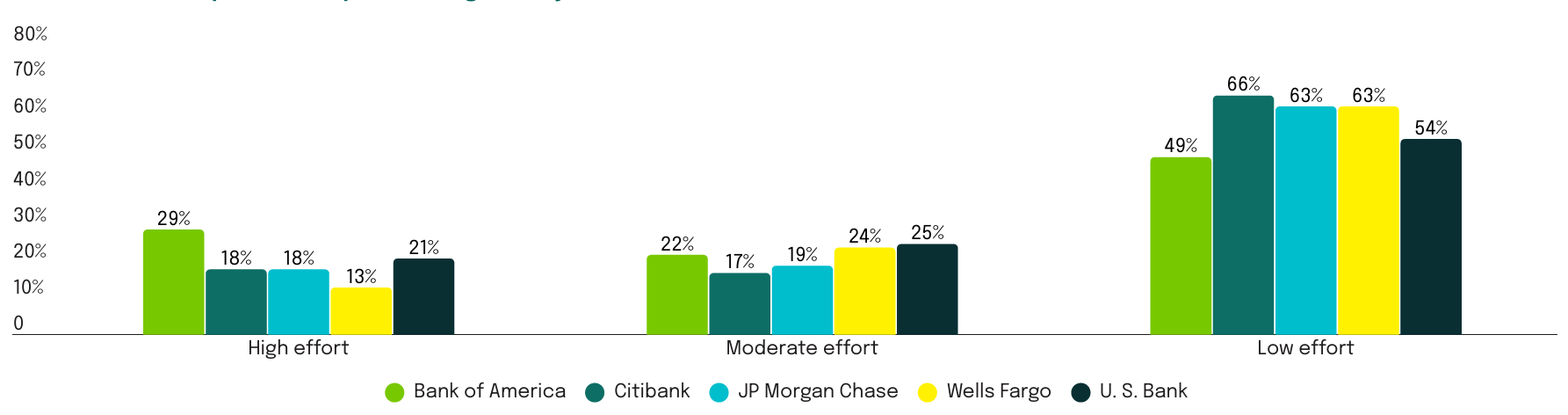

Ease and speed tell part of the story. Effort scores tell the rest. Even when an app is rated easy to use, customers still evaluate how much effort it takes to accomplish what they came to do. Low-effort experiences reduce friction. Whereas high-effort ones create the kind of quiet dissatisfaction that does not show up in quarterly satisfaction surveys until a customer is already out the door.

For perspective, Wells Fargo recorded the highest share of customers reporting low effort, with JPMorgan Chase and Citibank close behind. While, Bank of America showed the largest proportion of customers rating their experience as high effort at 29%, more than double JPMorgan Chase’s 13%.

(Sogolytics CX Rankings: U.S. Banking 2026): Customer effort required to complete banking tasks. Bank of America shows the highest share of high-effort ratings at 29%; Wells Fargo leads on low effort at 66%.

A 16-point gap in high-effort ratings between the best and worst performers is not a product quality gap. It is an experience design gap, and it shows up directly in switching intent.

Trust is Strong but Not Unconditional

Across all five banks, trust in data protection is high. Between 78% and 84% of customers agree that their bank protects their personal and financial information. Confidence in digital tools sits in a similar range, with JPMorgan Chase leading at 89%.

Where the numbers get more nuanced is a harder question: does your bank act in your best interest? That figure tops out at 75% for U.S. Bank and drops to 71% at Bank of America. These are still majority scores, but they represent a softer form of trust, one that is easier to erode.

A 25-30% trust deficit on the question of institutional alignment is not a crisis. But it is a signal. Banks that operate purely transactionally, without proactive communication, transparent fee structures, or service that anticipates member needs, are accumulating goodwill debt that will eventually come due.

This dynamic is well-documented in credit union CX research as well. Our post on reputation management for credit unions examines how member trust is built and lost across public-facing and service touchpoints.

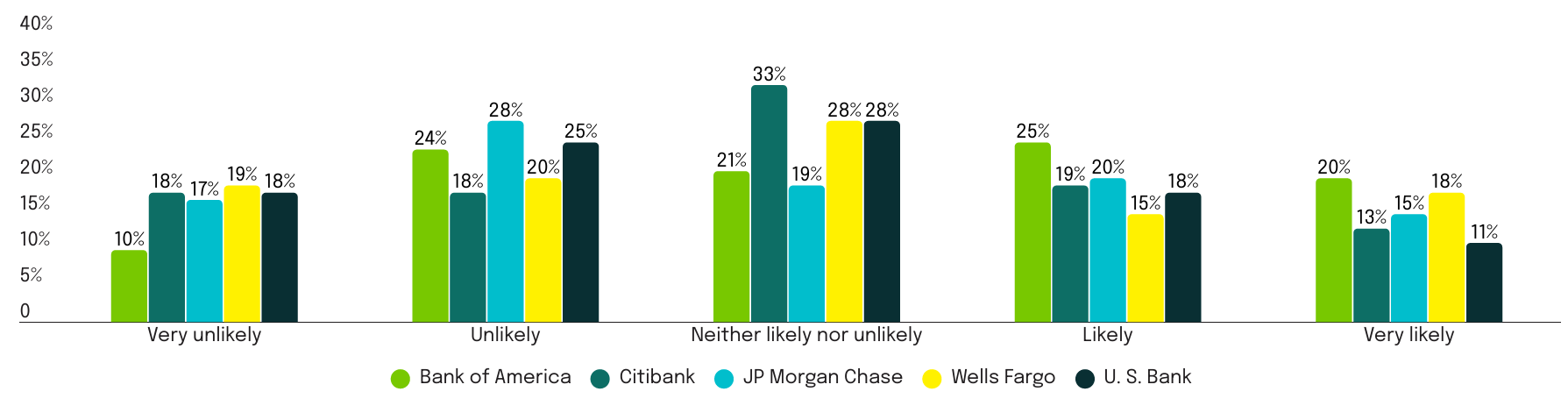

Switching Intent: A Leading Indicator, not a Lagging One

Perhaps the most operationally significant finding in the report is around switching behavior. While most customers report positive overall experiences, roughly one third say they would be likely or very likely to switch banks if a competitor offered a noticeably better experience.

Bank of America shows the highest share of customers open to switching at 45%. JPMorgan Chase sits at 35%, Wells Fargo at 33%, Citibank at 32%, and U.S. Bank at 29%. The fact that the bank with the strongest overall CX scores still has 35% of customers open to switching is a useful reminder that satisfaction and loyalty are not the same thing.

(Sogolytics CX Rankings: U.S. Banking 2026): Likelihood to switch banks for a better experience. Bank of America shows the highest switching intent at 45%; U.S. Bank is lowest at 29%.

These customers are not already gone. They are evaluable. For competitors, this is a targeting signal. For incumbents, it is an early warning that satisfaction scores alone are not a sufficient proxy for retention risk.

A Practical Look at the Data: Regional Bank Scenario

Consider a regional bank with strong branch infrastructure but lagging digital tools. Its customers rate in-branch service highly, but mobile app ease scores sit in the low 70s compared to JPMorgan Chase’s 87%. In this study, switching intent at such institutions tends to be elevated.

That threshold matters. If your satisfaction scores are good, but your digital experience is merely average, you are in a structurally vulnerable position. Customers who feel fine but would switch if something better came along represent a segment that competitor acquisition campaigns can reach with relative ease.

The bank in this scenario does not need to rebuild its digital experience from scratch. It needs to understand where in the digital journey customers are encountering friction, which tasks are rated slowest or most effortful, and how those friction points correlate to the customers most likely to switch. That requires measurement, not guesswork.

Tools like SogoCX and Sogolytics’ Experience Navigator are built for exactly this kind of diagnostic work, helping teams move from awareness of a problem to a prioritized action plan.

5 Things the U.S. Banking CX Rankings Reveal for CX Teams

1. Mobile experience is the primary CX battleground

With 50% of customers banking mostly digitally, app ease and speed scores are now as consequential as branch satisfaction ratings. JPMorgan Chase leads both categories. If your app experience is below benchmark, that gap is visible to customers every time they open the app.

2. Branch visits still drive significant satisfaction signals

JPMorgan Chase records the highest share of very efficient branch visits at 55%. Even as digital dominates volume, branch interactions handle complex, high-stakes moments. Satisfaction from those interactions carries disproportionate weight in overall loyalty scores.

3. Digital self-service effectiveness separates good from great

59% of JPMorgan Chase customers say the bank’s digital tools help a great deal in completing tasks without staff assistance. Banks at the lower end of this scale are pushing customers toward support calls unnecessarily.

4. Switching intent is not a lagging indicator, it is a leading one

Bank of America shows the highest share of customers open to switching at 45%. These customers are not already gone; they are telling you they are evaluable. For competitors, this is a targeting signal. For incumbents, it is an early warning.

5. CX investment priorities need to align with what customers value

Security and service quality outrank rates and rewards at a ratio of roughly 3:1 in this study. CX budgets that do not reflect this hierarchy are solving the wrong problems.

What the Rankings Mean for CX Strategy

The Sogolytics CX Rankings: U.S. Banking 2026 is not a report about which bank wins. It is a report about what winning looks like, and what the distance between current performance and that benchmark costs in loyalty, switching risk, and advocacy rates.

The banks leading across these metrics have one thing in common: they have invested in understanding the experience customers are really having, not just the experience they assume they are delivering. That gap, between the experience a bank designs and the experience a customer lives, is where CX strategy earns its value.

The Experience Navigator framework from Sogolytics is designed to close that gap. Rather than relying on point-in-time satisfaction surveys, it maps experience signals across the customer journey, identifies where friction accumulates, and helps teams prioritize the interventions that will move both satisfaction and retention metrics. For financial services teams trying to translate this report’s findings into a diagnostic program, that is where the work starts.

Explore the full methodology and findings in the Sogolytics CX Rankings: U.S. Banking 2026 report.

Frequently Asked Questions

What does the Sogolytics CX Rankings: U.S. Banking 2026 report actually measure?

The report is based on a survey of 1,018 U.S. consumers who identified one of five major banks, Bank of America, Citibank, JPMorgan Chase, Wells Fargo, and U.S. Bank, as their primary institution. Respondents rated their experience across ease of completing tasks, speed, digital self-service effectiveness, branch experience, effort required, trust, and overall satisfaction. The study also captured loyalty indicators including likelihood to recommend and switching intent.

Which bank performed best in the 2026 U.S. Banking CX Rankings?

JPMorgan Chase leads across multiple dimensions in the study, including mobile app ease (87% rating tasks easy or very easy), mobile app speed (82%), digital self-service effectiveness (59% say tools help a great deal), in-branch ease (76%), and highest share of very satisfied customers overall. No single bank dominates every category, but JPMorgan Chase shows the most consistent performance across the key experience drivers measured.

How does customer switching intent in banking relate to experience quality?

The study finds that roughly one third of customers across all five banks would be likely or very likely to switch if a competitor offered a noticeably better experience. Switching intent is highest at Bank of America, where 45% of customers indicate openness to switching. This figure is not a measure of immediate churn risk; it reflects the degree to which customers are evaluable by competitors. Banks with high switching intent scores have a structural vulnerability that promotional offers alone are unlikely to close.

What do banking customers actually value most when choosing where to bank?

The top two factors are good customer service and support and security of personal and financial data, each cited by 36% of respondents. Easy ATM access ranks third at 34%. Competitive interest rates and personalized offers rank near the bottom of the priority list, at 13% and 8% respectively. This finding suggests that many banks are investing their CX budgets in the wrong place, optimizing for financial incentives while underinvesting in service quality and security experiences that customers weight more heavily.

How should financial institutions use this benchmarking data to improve CX?

Benchmarking data like the U.S. Banking CX Rankings is most useful as a diagnostic starting point, not an endpoint. The report identifies where gaps exist between leading and lagging institutions across specific experience dimensions. The next step is internal measurement, understanding where your own customers experience friction, and mapping that friction to loyalty behavior. Tools like SogoCX and the Experience Navigator framework help financial services teams connect survey data to customer journey signals and prioritize improvements based on their actual impact on retention and satisfaction scores.

Does the report address differences in how customers bank across age groups?

Yes. The data shows clear generational patterns both in bank preference and banking behavior. Among consumers aged 18 to 24, U.S. Bank holds the highest share at 36%. JPMorgan Chase leads among 25- to 34-year-olds. On banking behavior, digital dominates across all age groups, but branch reliance increases steadily with age. Among respondents 65 and older, 46% still bank mostly digitally, but 25% report primarily banking in branch, the highest share of any age group. Financial institutions need to support both channels effectively rather than treating digital as a replacement for physical service.