A few years ago, a brand taking a public stance on a social or political issue felt bold. Today, it feels unavoidable. Boycotts trend overnight. Stock prices move with headlines. And consumers across the political spectrum are making deliberate choices about where they spend based on what a brand stands for or what it is perceived to stand for.

The challenging piece for companies is that in many cases, a brand does not choose a position. Someone else chose it for them.

We set out to understand just how much this is affecting consumer behavior. Sogolytics conducted a national survey of 1,014 U.S. adults, examining how corporate political and values-based signals influence trust, loyalty, and spending. The findings are worth paying attention to, no matter where your brand sits on the engagement spectrum.

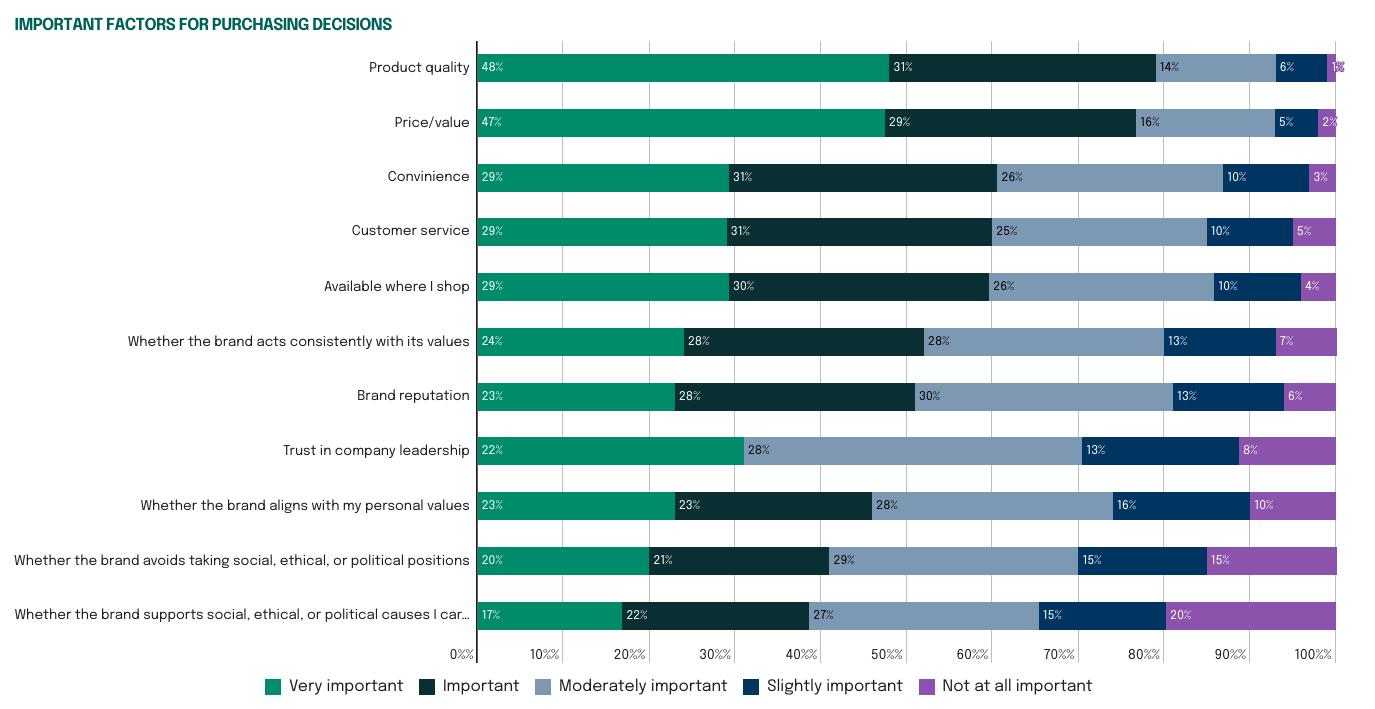

Product Quality Still Leads. But it No Longer Locks in Loyalty

When we asked what drives them to stay loyal to a brand, consumers unsurprisingly ranked product quality (79%) and price (76%) at the top. Surprisingly, 51% said even if a brand offers a great product, they would stop buying if they strongly disagree with what it stands for

“Product experience may still open the door. But a brand’s values can close it.”

Sogolytics, Consumer Brands and the Risk of the Political Stance, 2026

Also, values-based factors, including consistency with values (52%), brand reputation (51%), trust in leadership (51%), and alignment with personal values (46%), now influence roughly half of all purchasing decisions. That is not a fringe behavior; it is a mainstream reality.

The Financial Risk is Asymmetric, And it’s not Small

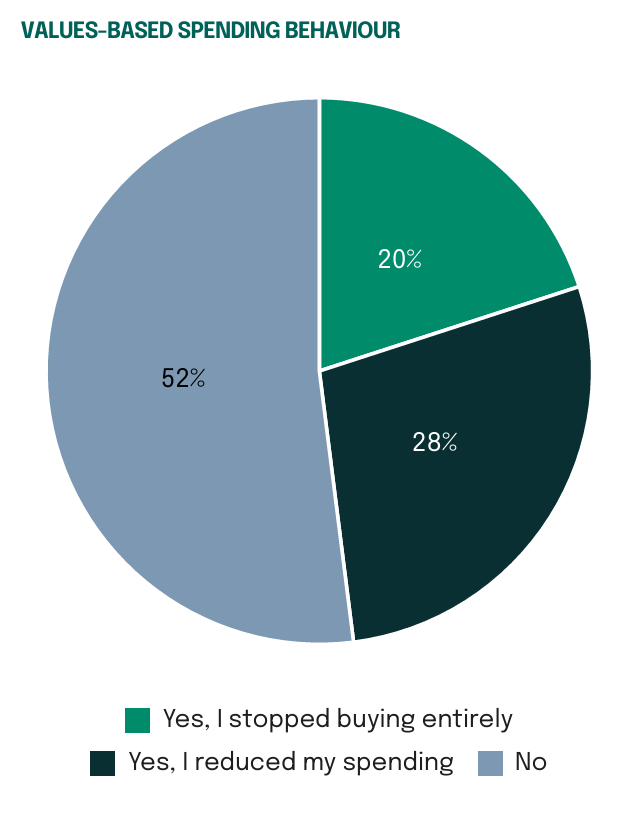

Reputational risk does not play out equally in both directions. The downside hits harder and more often than the upside.

Nearly half of survey respondents (48%) said they reduced or stopped spending with a brand in the past 12 months, specifically because of its values or public behavior. Only 9% said they increased spending for the same reason.

That is roughly a 5:1 ratio, and it points to something brands cannot afford to ignore: the financial downside of a perceived values misalignment is significantly larger than the upside reward of getting it right.

This asymmetry also shows up in how consumers describe their actual behaviors too. For context, 23% bought less from a brand, while 20% boycotted one outright. And, only 9% spent more. The pattern is consistent across political affiliations, which brings us to one of the more counterintuitive findings in the data.

The Values-driven Consumer Defies the Stereotype

There is an assumption in marketing that values-based consumption is driven primarily by women and progressive consumers. The data challenges this.

Republicans (50%) and Democrats (49.8%) reported reducing their spending with brands they disagreed with at nearly identical rates. Republicans were slightly more likely to stop buying entirely (26.4% vs. 23.2% for Democrats).

And by gender: 50% of men reduced or stopped spending compared to 45% of women. Men also boycotted brands at a higher rate (21% vs. 18%) and bought less at a higher rate (25% vs. 21%).

High earners are also more active. Seventy-four percent of households earning between $150K and $199K reduced or stopped spending with a brand based on its ideological position, versus 41% of households under $25K. Changing your spending based on values is, in part, a reflection of having the financial flexibility to do so.

“The values-driven consumer is not a demographic segment. It is a behavioral pattern that crosses party lines, gender, and income.”

Sogolytics, Consumer Brands and the Risk of the Political Stance, 2026

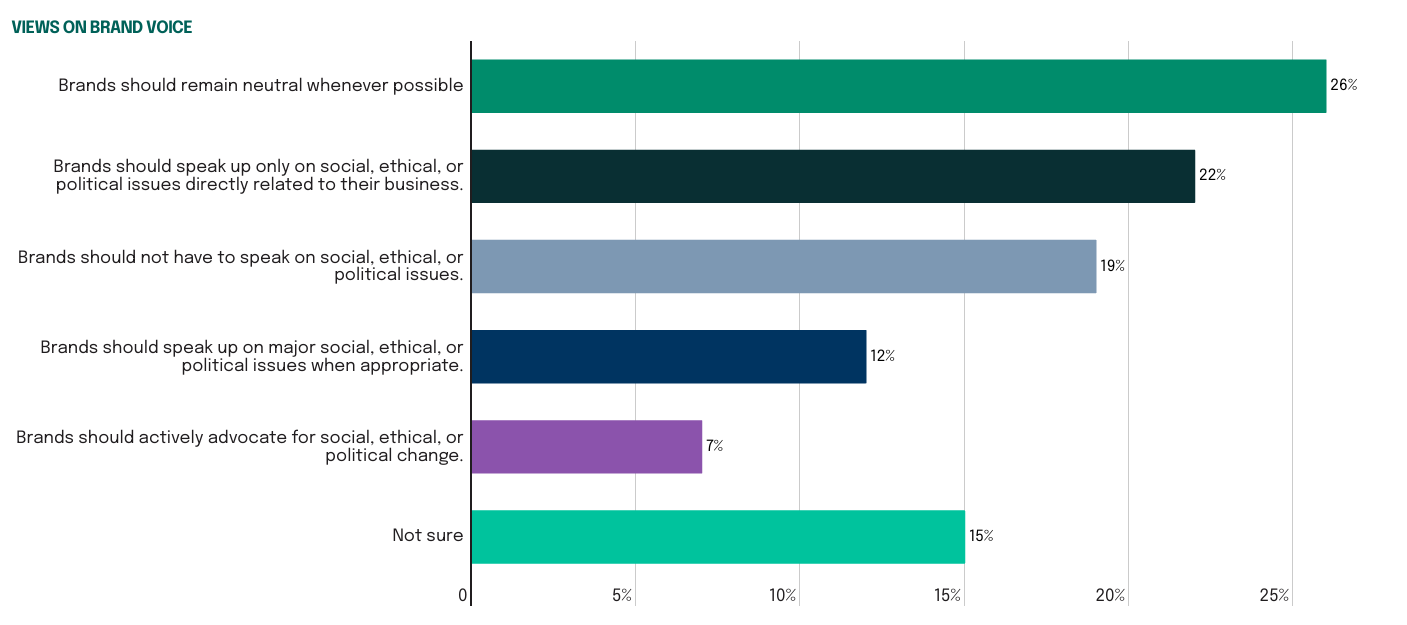

Most Consumers Still Want Brands to Stay Out of Politics

Many consumers want brands to stay neutral; almost half (45%) felt that brands should not speak out on social, ethical, or political issues or should stay neutral whenever possible. Forty-one percent felt brands had some duty to engage, and 15% were unsure.

The picture differs by group. Sixty percent of Republicans felt brands should stay neutral, compared to 36% of Democrats. Support for brand neutrality also rises with age, climbing from 22% among 18 to 24-year-olds to 60% among those 65 and older.

When Brands are Vocal Authenticity Matters More than Agreement

Among consumers who said they are open to brands engaging on issues, the top two things they look for are authenticity (36%) and transparency (34%). Whether they personally agree with the brand’s position ranked much lower, at just 17%.

Consumers are not primarily asking whether a brand shares their politics. They are asking whether the brand means what it says.

Which is why 56% of all respondents said they care more about whether a brand is authentic than whether they agree with every position it takes. 55% said they are skeptical when brands speak about causes without taking real action to back it up.

“Authenticity outranks agreement. Consumers notice the gap between words and actions faster than most brands realize.”

Sogolytics, Consumer Brands and the Risk of the Political Stance, 2026

Democrats and Republicans weigh authenticity slightly differently. Democrats ranked transparency (42%) and authenticity (41%) highest. Republicans prioritized leadership credibility (23%) and relevance to customers (24%). But both groups share the same underlying expectation: if you are going to speak, your track record needs to back it up.

Brands Rarely Control the Narrative About How Their Values are Perceived

One of the most practical findings in this report has nothing to do with whether a brand should take a stance. It has to do with how consumers find out about one.

Half of consumers (50%) learn about a brand’s social or political positions from social media. Another 42% hear about them from news media. Only 23% hear about them directly from the brand itself.

This means that for most brands, the values narrative is already being written by someone else. Social media users, journalists, and influencers are shaping perception before the brand has even decided how to respond. And two-thirds of consumers (66%) agree that brands should expect customer backlash when they take controversial positions, a view held by 73% of Democrats and 72% of Republicans alike.

The implications are clear: If you are not actively monitoring how your brand is perceived, you are ceding the narrative to whoever is loudest, not whoever is most accurate.

What this Looks Like in Practice

To see what this looks like beyond the survey data, it helps to look at how these patterns have played out for actual brands. Target’s stock dropped 33% across the first three quarters of 2025, a period marked by consumer boycotts and broader macro pressures. Whether or not any single campaign was the primary cause, the period illustrated how quickly public perception can translate into measurable financial impact.

Bud Light’s 2023 partnership backlash is another example. Sales dropped 25% overall, and the brand lost its position as America’s best-selling beer for the first time in over two decades. What made the damage harder to contain was not just the initial reaction, but how long it lasted. Eight months after the backlash began, sales were still down 32%. It illustrated how quickly a single perceived misstep can translate into sustained, measurable financial loss.

These are not cautionary tales about having the wrong values. They are cautionary tales about the gap between what a brand signals and what it backs up with behavior.

Get The Full Picture

This blog draws on select findings from our full research report, Consumer Brands and the Risk of the Political Stance. The complete report includes demographic breakdowns by age, income, gender, and political affiliation, data on which industries consumers expect to engage versus stay neutral, and a closer look at which specific issues drive the most intense consumer responses.

If your team is navigating brand communications, reputation monitoring, or customer experience strategy in a politically charged environment, the data is worth having.