Reputation is Now an Operational Metric

For decades, credit union reputation was something that lived almost entirely in personal conversations. Members recommended their credit union to family members at the dinner table, neighbors mentioned it at community events, and trust passed quietly from one generation to the next. It was a slow, durable kind of reputation, and almost none of it was ever measured.

That status quo no longer holds. Banks have moved beyond the teller desk into WhatsApp, in-app chat, and proactive outreach, while members increasingly form their opinions online before they ever walk into a branch. A credit union’s first impression is now shaped by Google reviews, social media comments, branch ratings, app store stars, and search engine results, most of which are visible to every prospect who searches for you, often before they ever visit your website.

The result is that reputation management can no longer live inside the marketing team alone. It has become an operational discipline that sits at the intersection of member experience, employee experience, and brand, with every interaction either building trust or quietly draining it.

Why Credit Unions Are Particularly Exposed

Credit unions have always competed on trust. Members choose them over big banks because they expect a different relationship; one built on community, fairness, and genuine service. When public sentiment around a credit union starts to soften, the differentiation softens with it.

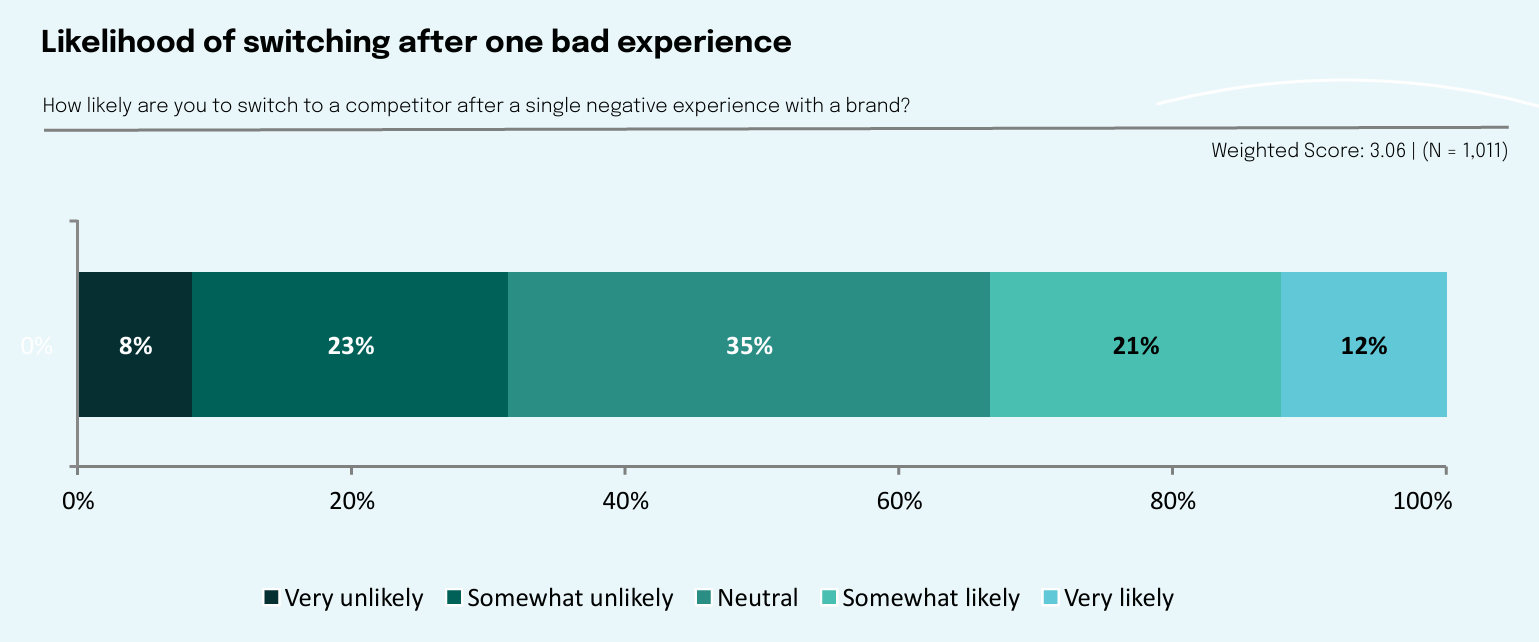

Sogolytics’ CX Index 2026 found that more than half of consumers, across industries, say a single poor interaction can permanently affect their trust in a brand. Nearly as many will switch providers if issues remain unresolved. For credit unions, that signal carries extra weight, because trust isn’t a product feature; it’s the entire foundation of the member relationship.

Younger members research before they join, lean on reviews, and are more likely to share a negative experience online than to call you about it. A single bad review from a frustrated member can sit at the top of search results for months, shaping how dozens of prospects feel about your brand before they ever speak to a staff member.

The FOUR pillars of credit union reputation management

Reputation management is not just review-monitoring. It is a coordinated discipline built on four pillars that work together.

1. Listen across every channel members use

Members and prospects form opinions across more channels than most credit unions actively monitor. Google and Facebook are usually covered. App store reviews, branch-level Yelp pages, banking forums, and local community groups often are not. A complete listening setup pulls signals from every source members and prospects, and not just the low hanging fruits.

2. Route feedback to the team that can act on it

Speed of routing decides whether a reputation signal becomes a fix or a future review. A negative branch review needs to reach the branch manager within hours, not weeks. A pattern of complaints about the mobile app belongs to the digital team. Reputation systems that cannot route feedback effectively end up as alert systems no one acts on.

3. Close the loop with members publicly

Public responses to negative feedback are read by far more people than the original complainant. When a member shares negative feedback in public, a thoughtful response demonstrates accountability to everyone watching. The CX 2026 report found that customers value clear and transparent communication (25%) and trustworthiness (25%) as top experience factors. A well-handled response to a negative review can earn more trust than a hundred positive ones.

4. Connect reputation signals to operations

Reputation data is operational data wearing a different name, and this is the most overlooked pillar of the four. A consistent stream of negative reviews about wait times, fees, or staff friendliness is operational data, not just a marketing problem. Those signals should feed back into branch staffing, training, fee structure reviews, and digital roadmap planning.

5 Types of Reputation Risk Credit Unions Face

Knowing the failure modes helps you build defenses against them. These FIVE recurring patterns show up across credit union reputation programs:

1. The unresolved complaint that goes public

Small service failures turn into public reputation problems when nobody follows up in time. A member calls about a fee dispute, but nobody calls back. Two days later, a 1-star Google review appears with the full story. The original problem could have been fixed in 10 minutes. The public version now lives forever.

2. Branch-level inconsistency

A credit union’s reputation is only ever as strong as its weakest branch. One location may have glowing reviews, while another ten miles away has a trail of complaints about wait times and staff attitude. Members searching for the credit union see both, and the gap between them erodes confidence in the brand as a whole.

3. The digital outage handled badly

Outages are inevitable, but how they get communicated decides whether the reputation hit lasts hours or months. Mobile banking goes down for two hours. No status page, no proactive communication, no apology email. App store reviews drop by half a star overnight, and they take months to recover.

4. The frontline turnover spiral

Service quality follows staff continuity, and most members feel the change before they can name it. Long-tenured tellers leave. Newer staff don’t yet know the members, the policies, or the workarounds. Service quality dips, members’ notice, reviews soften, and the brand starts to feel less personal than it used to.

5. The fee surprise no one explained

Communication failures around fees create reputation damage that the fees themselves never would. Let’s say a credit union rolls out a new fee structure, raising the minimum balance for free checking or adding a maintenance charge to dormant accounts. The change is disclosed in a routine email update, technically compliant but buried under several paragraphs of unrelated information, and most members never open it. More often than not, members only end up knowing about the fee once their statement arrives. While the fee itself may have been reasonable. The way members learned about it was not. Such complaints generally end up on social media, creating unnecessary and avoidable outrage.

Where Reputation Breaks for Credit Unions

The most common failure is treating reputation as defensive. Credit unions respond to negative reviews but rarely build systems that proactively encourage positive ones from satisfied members. The result is a public reputation skewed by the loudest complainers, while the majority of happy members never speak up.

Another common gap is the disconnect between what members say privately in surveys and what they say publicly online. A member might rate their loan experience 9 out of 10 in your post-transaction survey, then never leave a Google review. Building a clear path from positive private feedback to public advocacy is one of the highest-leverage reputation moves a credit union can make.

A Use Case: When Reputation Listening Surfaces An Operational Fix

Consider a mid-sized credit union with strong NPS scores but a 3.4-star Google rating on its flagship branch. Leadership assumed the reviews were outliers from a few frustrated members. A structured listening review showed a different pattern.

Of the 47 negative reviews over the previous year, 31 mentioned the same three issues: long wait times on Saturday mornings, confusing signage at the new drive-through, and a specific teller who repeatedly received complaints. None of these were marketing problems. They were operations problems showing up in a marketing channel.

Once the credit union added a Saturday-morning floater, redesigned the drive-through signage, and addressed the staffing issue, the review score climbed from 3.4 to 4.2 over the next two quarters. The lesson: reputation data is operational data in a different format, and the credit unions that read it that way see the fastest improvements.

Conclusion

This article has covered a lot of ground: how reputation became operational, why credit unions are exposed in particular, the four pillars of a working program, the five types of risk to watch, and where most programs break down. Reputation management at a credit union is no longer about responding to bad reviews. It is about building a listening, routing, and operational-response system that turns public sentiment into a strategic asset.

Sogolytics’ Experience Navigator was built to give credit union leaders a structured way to do this work without starting from a blank page. The four-step setup, industry and vertical, business model, operational scope, and objectives, configures the platform to the specific shape of a credit union’s operation. From there, it maps the digital, physical, process, and human touchpoints that drive member sentiment, and recommends the right feedback method and metric for each one, so the reputation signals you collect arrive with measurement attached. Branch managers, digital teams, and member service leads can each see their segment of the reputation map alongside the others, which is what turns a reputation dashboard from a slide into an operating tool.

While listening across channels is only half the job done, the real value comes from acting on what reputation signals reveal, every week, across every team that shapes the member experience. That is where most credit unions need a partner, and where Experience Navigator earns its place in the stack.

FAQs About Credit Union Reputation Management

What is reputation management for credit unions?

What is reputation management for credit unions?

Reputation management for credit unions is the structured practice of monitoring, responding to, and learning from what members and prospects say about the credit union in public channels. That includes Google reviews, social media, app store ratings, banking forums, and local community groups. It is no longer a marketing-only function, because the patterns that show up in public sentiment usually trace back to operational issues that need branch, digital, or service-level fixes.

How important are online reviews for credit unions?

Online reviews carry significant weight, especially for younger members. Most prospects now research a credit union online before joining, and the first three results on Google often shape their initial impression. A 4-star average versus a 3.5-star average can be the difference between a prospect walking in and a prospect picking a different institution. Reviews also influence existing members during moments of doubt, like when they are considering whether to move their primary deposit relationship.

How should a credit union respond to a negative review?

Respond quickly, publicly, and personally. Acknowledge the issue without making excuses, take the conversation offline for the specifics, and follow up internally on the root cause. A thoughtful response signals to everyone reading that the credit union takes member feedback seriously. The CX 2026 report found that transparent communication and trustworthiness are among the top drivers of positive experience, so how you handle a complaint often matters more than the complaint itself.

What is the difference between reputation management and customer service?

Customer service handles individual member issues as they happen. Reputation management looks at the patterns across many service moments and asks what they say about the credit union as a whole. A single complaint is customer service. Forty-seven complaints about the same branch over a year is a reputation signal, and it usually points to an operational fix that customer service alone cannot make.

How often should a credit union review its reputation signals?

Most credit unions review their reputation data weekly at the team level and monthly at the leadership level. Branch-level reviews and individual review responses should happen within 24 to 48 hours of posting. Quarterly, the patterns should be reviewed against operational data, like wait times, branch staffing, and digital performance, to see where reputation signals are pointing to systemic issues.

Can private survey feedback be turned into public reviews?

Yes, and most credit unions under-invest in this. A member who scores you 9 or 10 on a post-interaction survey is a strong candidate for a public review. A short, well-timed prompt that invites them to share their experience on Google or their app store of choice can meaningfully shift your public review mix. The path from private satisfaction to public advocacy is one of the highest-leverage moves a reputation program can make.